5C Wealth Review and Outlook — January 2025

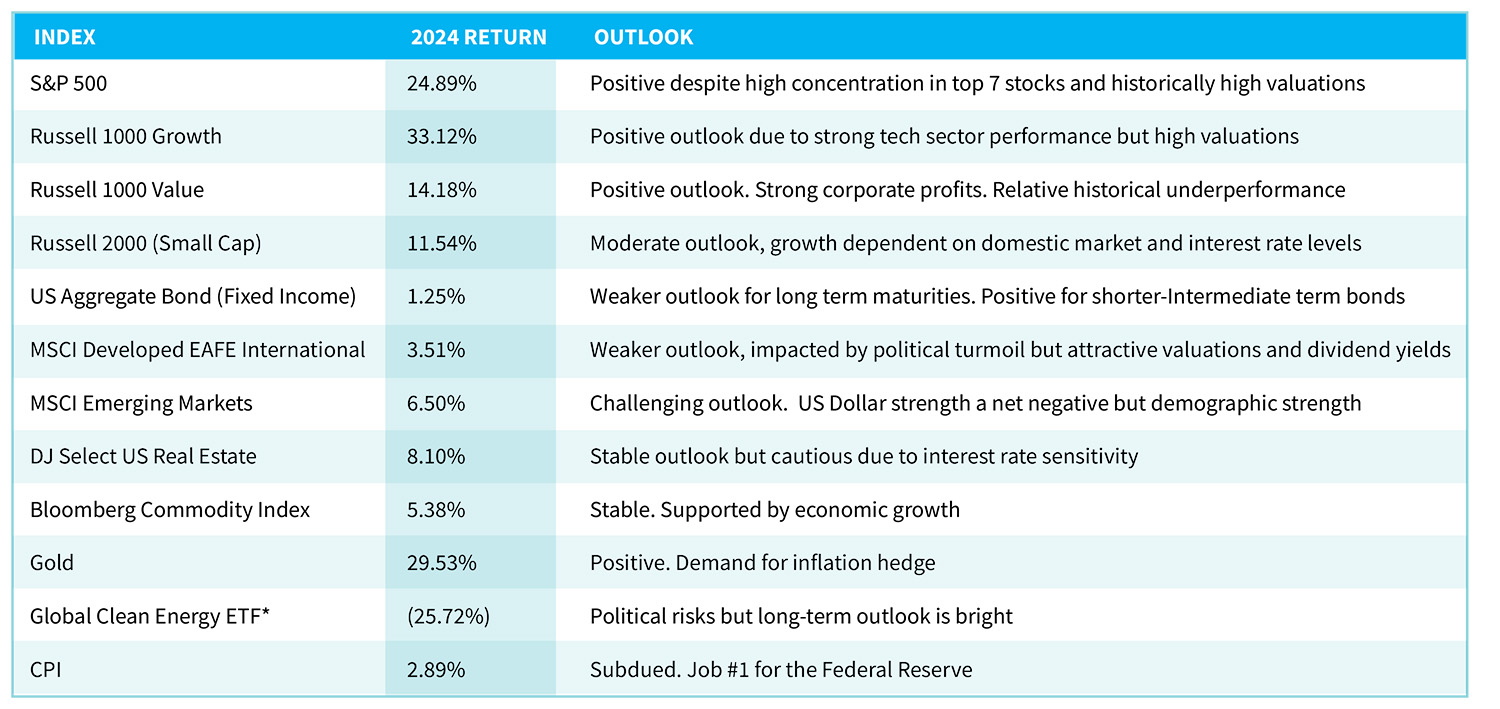

During 2024, financial and global capital markets were heavily influenced by the Federal Reserve and monetary policy. Initially, the Fed signaled that short-term interest rates were too high and gradually cut rates throughout 2024. However, further cuts were tempered by a resilient US economy and inflation exceeding the Fed’s target. Despite the interest rate uncertainty, the S&P 500 gained over 20% for the second consecutive year. The gains were led by technology stocks focused on Artificial Intelligence – note in the chart below the domestic growth and gold led rally.

Sources: Morningstar, Bloomberg LP * S&P Global Clean Energy Index

Investors continue to struggle with inflation fears and the Fed’s interest rate policy. Higher interest rates impact all borrowers, whether those seeking a mortgage, corporations borrowing for business purposes, or the US government refinancing its growing debt. During much of the last 15 years, the global economy enjoyed a relatively low-interest rate environment; industry now needs to learn how to operate in a “higher for longer” future and accompanying tradeoffs.

The US economy appears poised for continued economic growth and increasing profits, despite continuing conflicts in Ukraine and the Middle East. In fact, the aerospace and defense sector has been particularly strong as the corresponding ETF (“ITA”) returned 15.8% in 2024 and is up over 7% in the new year. However, economic growth ex-US does not look as robust. China, the 2nd largest global economy, has many economic concerns, including a weak real estate market, high youth unemployment, slowing economic growth, and worsening US trade relations. Several other developed world economies have noticeably weakened, including the UK, France, and Canada.

US Employment and Monetary policy

Domestically, employment has remained robust; 256,000 non-farm payroll jobs were added in December. The unemployment rate edged down to 4.1%. This is consistent with a “full employment rate”, the low end of the natural rate of unemployment which ranges between 4% and 6%. Notable job gains occurred in the health care, government, social assistance, and retail trade sectors.

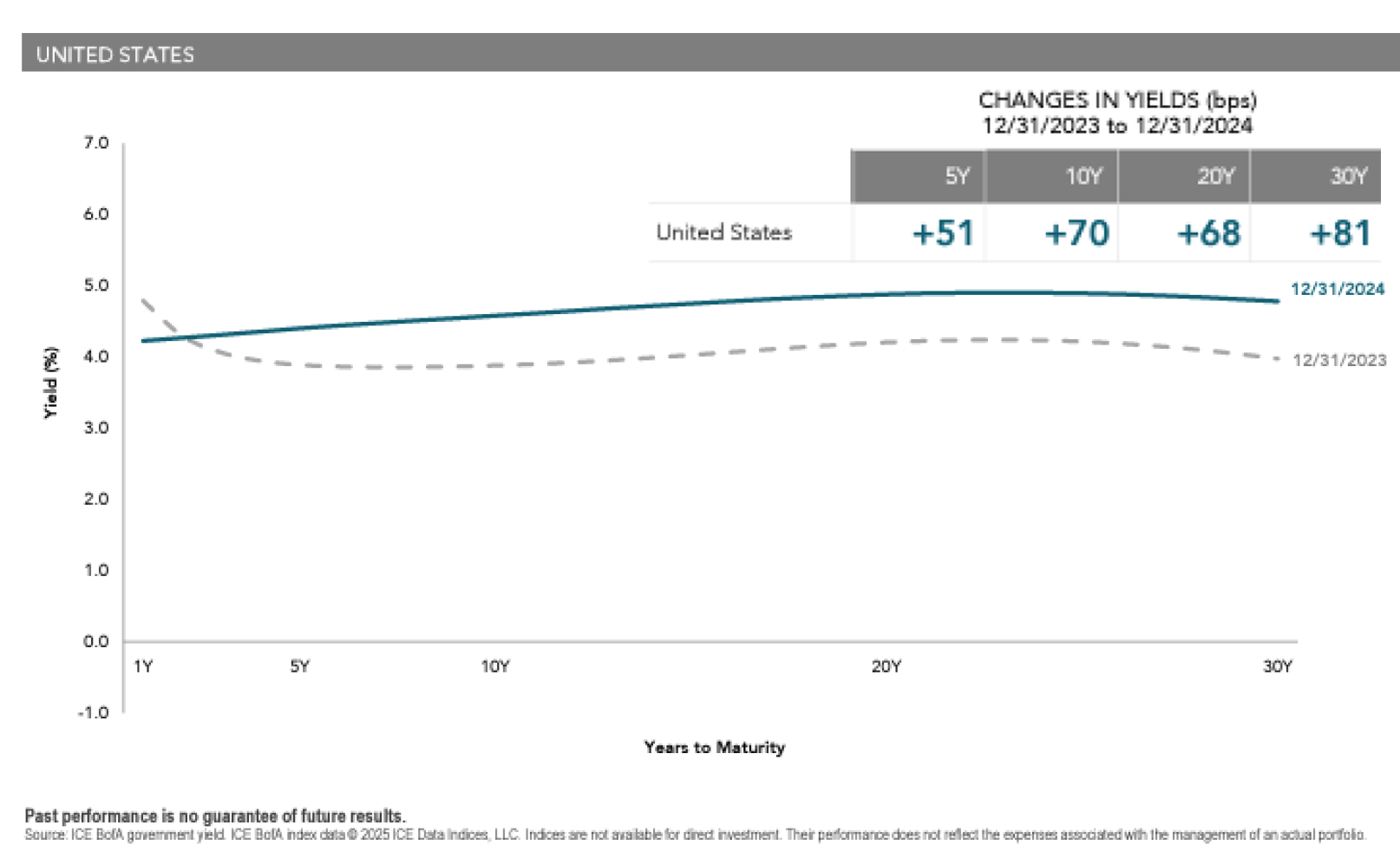

The futures market, a popular rate forecasting tool, anticipates the Fed will modestly lower rates (by 25 – 50 basis points) during 2025, indicating that this easing cycle might be ending. Long-term securities experienced more significant movement, the 10-Year US Treasury yield rose from 3.6% to 4.6%, which corresponds to a price decline of 7.7%.

These macroeconomic developments underscore the complex interplay between monetary policy, inflation, and economic resilience. With short-term interest rates stabilizing, we focus on the new administration’s fiscal policy.

Professionals and armchair quarterbacks alike have rushed to predict winning and losing sectors during Trump’s second administration. For example, stocks of private prison/security companies spiked as the threat of mass deportation loomed. Conversely, clean energy companies were negatively impacted by Trump’s aversion to government subsidies. We believe that many of these knee-jerk reactions will be misguided – the effect of new policy is often not instantaneous. However, it is important to acknowledge the new administration’s goals and how our clients may benefit from new policy.

Debt and Taxes:

During 1992, straight-talking Ross Perot campaigned for US President, focusing on reducing the national debt. He likened debt to: “the crazy aunt we have in the basement, everyone knows she’s there, but nobody talks about her”. The debt was 45% of GDP in 1992, currently it is approaching 125%. Objectively and obviously, the problem has worsened. The inherent conflict in two of Trump’s main goals is concerning: extending tax cuts from the prior Trump administration AND reducing the national debt. Of the $6.75 trillion the US government spent during 2024, $1.8 trillion would have to be cut in 2025 to “balance” the budget. The appointment of a special commission tasked with reducing government spending may yield useful ideas. However, cooperation from Congress, strategic implementation and actual cost savings may prove much more difficult in the short term. Those in power tend to want to remain so. Since, the vast majority of government spending is non-discretionary what local politician wants to be a poster child for efficiency, but a lost next election? We certainly hope that DOGE implements significant cuts to the pork rolling around the budget. However, tax cut extensions without greater net growth and spending cuts may lead to much finger pointing and an increased deficit.

Tariffs & Regulation:

Are tariffs a gateway to another inflation cycle or a savvy negotiating tool? During Trump’s first term, total tariffs collected rose from $34.6 billion to $70.8 billion. Impressive, but only representative of 0.3% of our $30 trillion US economy. We are hopeful that threats are sufficient to foster useful changes to agreements with our trading partners rather than spark a trade war which disproportionately affects those least prepared to shoulder resulting increased costs. The new regulatory environment - a nod to “laissez faire” aims for “Sensible Regulation” vs. “Regulatory Overreach”. Future regulation should spur efficiency and disinflation. Regarding the many immigrants that reside here - be wary of the “cobra effect” of mass deportation. The supply of immigrant labor may very well help moderate labor costs and keep inflation in check.

Outlook for 2025 & Beyond:

We continue to maintain a strong weighting in growth stocks and technology sector. Near term, we expect they will continue to lead earnings growth within broad equity markets. As strategic long-term investors, we complement growth assets by adding to underperforming sectors and trimming the most appreciated investments. Traditional valuation metrics such as Price to Earnings or Price to Book ratios indicate that US large cap investments are overvalued. If the trend continues, a cyclical market selloff may bring the next “entry point” for these assets. Through our process of disciplined rebalancing, we focus and add to underperforming sectors that have become relatively attractive.

Consider fixed income: During 2024, the Aggregate Bond Index returned 1.25%; well below its 30-year average return of 4.56%. Despite the near term adjustment, we expect bonds to maintain their role as a positive stabilizing force in a balanced portfolio. Currently, bonds typically yield a tax adjusted return between 4-5%; with limited interest rate risk given our modest duration profile. The shifting yield curve is evidenced by the chart below.

Within the equity markets, health care and biotechnology stocks have underperformed the broader S&P 500 Index by more than 20%. We attribute this to a number of factors including government pressure on drug prices, post-pandemic vaccine demand declines, and, excepting weight loss drugs, an unclear new product pipeline. However, new product innovation continues, specifically within gene editing and precision medicine. We believe that cheaper valuation on health care companies will lead to outperformance in their equity prices over time. Growth through acquisition has historically been popular strategy within the health care space and we expect the new administration to be more accommodative to this support this strategy. The more flexible regulatory framework combined with depressed valuations, should provide additional support healthcare related companies both large and small.

Despite longer term weakness, we continue to maintain a material weighting in non-US equities (developed and emerging markets). They provide significantly cheaper valuations, diversification and a robust yield. Certain emerging market countries are experiencing rates of growth and consumption in excess of the domestic market. Our portfolios’ exposure to these sectors are at the lower end of our models; we expect to add to this asset class as their outlook improves.

Despite strong support from the prior administration, clean energy companies have performed poorly. As much as the new administration touts their support of fossil fuels, and executive pushback notwithstanding, we expect demand growth and will maintain our modest sector exposure. Accelerating growth in AI energy usage should create additional demand requiring alternative sources.

Cryptocurrency has enjoyed robust success and has been embraced by the new administration. We generally limit our direct exposure here and seek investment opportunities in related technology and other sector innovations.

We remain true to our investment process - the changing of the guard in Washington, or new technological innovation notwithstanding. We are cognizant of the strong two-year returns in equity markets, but also acknowledge a stable and growing US economy. Most importantly, we seek to evaluate and effectively manage the risk level assumed by each of our clients. We thank you for your continued support and wish everyone a healthy and prosperous 2025.

5C Capital Investment team.