5C Wealth Review and Outlook — November 2025

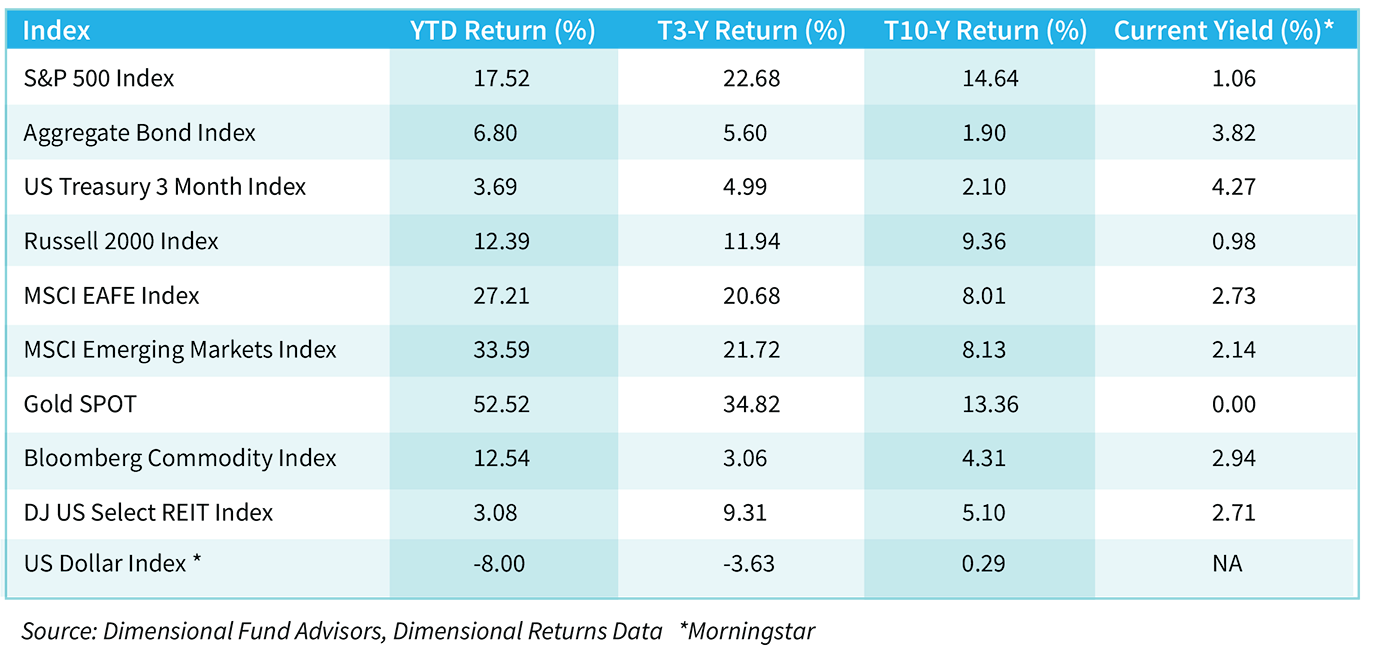

As 2025 closes, a variation of a classic Dickens line comes to mind: “It is the best of times, it is the uneasiest of times”. One look at the asset class returns shown in the table above gives a good idea why. The returns have been unambiguously strong across almost all asset classes for this year as well as the prior two. From the benchmark S&P 500 Index at +17% for the year and +22% annualized over the past three, to the Aggregate Bond index which is + 6.8% and +5.6% for the same periods, investors have been enjoying material positive returns across the risk spectrum. Even the hyper risk-averse camped out in US T-Bills have enjoyed a +3.7% and a +5% return over the year-to-date and trailing 3-year periods. These returns have spanned a change in Presidential Administrations, a monetary policy shift to lowering rates despite above-target inflation readings, and a tariff policy that, for whatever one may think of its merits, left final rates in perpetual flux.

Investment Results for period ending October 31, 2025

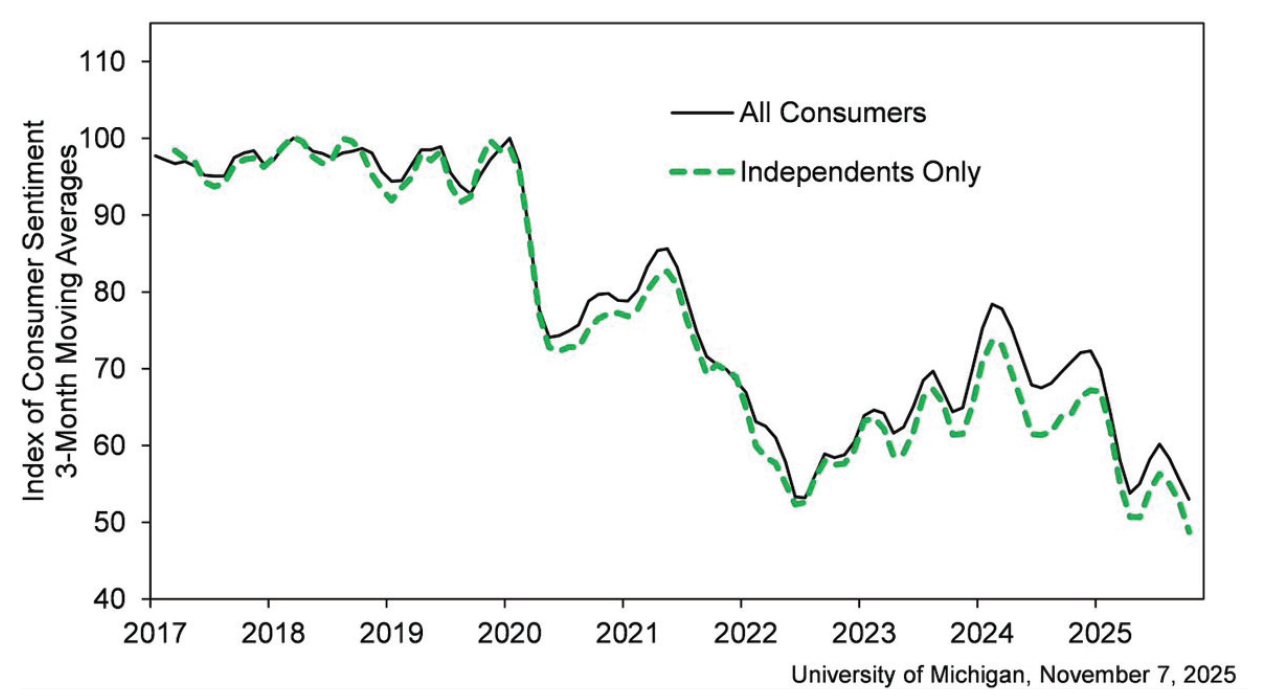

Why the unease? The University of Michigan Consumer sentiment index declined 6% this month and is almost 30% lower than a year ago. Consumer sentiment in November was led by a 17% drop in current personal finances and an 11% decline in year-ahead expected business conditions. With the federal government shutdown (now finally resolved) dragging on for over a month, consumers express concerns about its negative impact on the economy. The decline in sentiment was widespread amongst all major demographic groups - age, income and political affiliation. One notable exception: consumers with the largest tercile of stock holdings posted an 11% increase in sentiment, supported by continued strength in equity markets. The chart below expresses very low sentiment among consumers.

National Sentiment Trends, Including Recent Declines, Remain Fully Aligned With Views of Independents

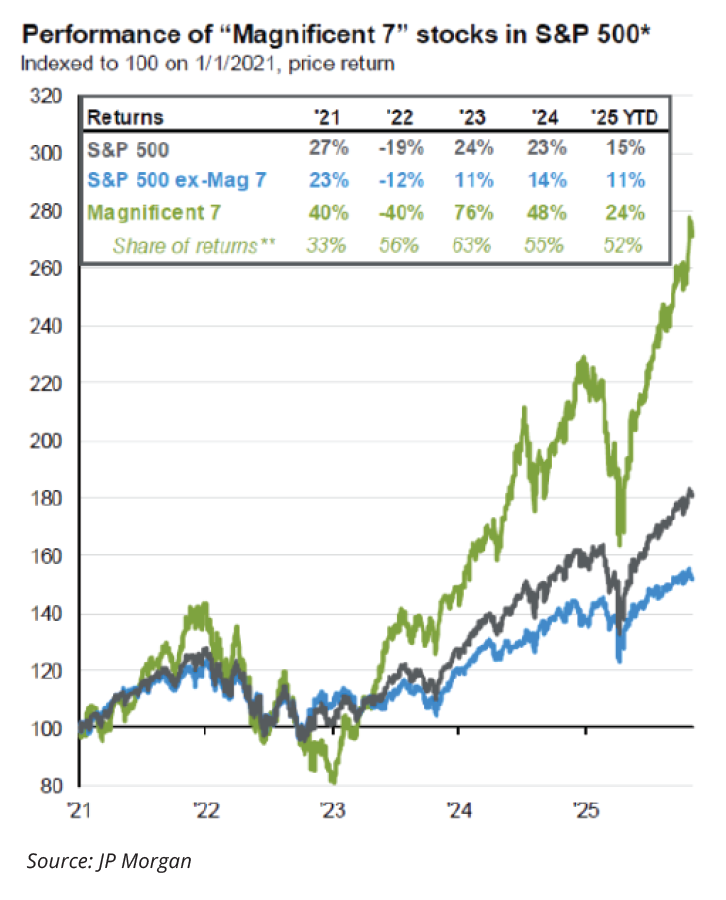

From a macro perspective, asset prices never continue straight up forever. A reversion to the mean is an inevitability even though its cause and timing may be unknown. Digging a bit deeper, one sees the highly concentrated nature of the returns of the large capitalization equity indices. The S&P 500, market cap weighted index has 7 companies representing almost 37% of the value while an equal weighted version of the index has lagged by over 9% this year. If these so called “magnificent 7” stocks should falter the overall index would certainly be in trouble. In times where economic growth is more robust small-cap stocks tend to lead the way. The Russell 2000 equity index of small cap stocks (still respectable 12% YTD) trails it large-cap peers by greater than 5%.

The chart on the right contrasts the performance of Magnificent 7 (top 7 names in S&P 500) vs. the other 493 stocks. The difference is staggering and reminiscent of “Nifty 50” from 1960’s.

Inflation - the perennial scourge of asset value, continues to run above the Federal Reserve’s stated targets. However, the Fed currently seems more focused on the labor market. Gold, the traditional inflation hedge; has enjoyed record returns, indicating that the markets remained concerned about inflation. Despite falling interest rates, the devaluation of the US dollar (greater than 10% during the first half of 2025) and recent federal legislation confirming the US Government’s commitment to additional deficit financing, indicates that debt service requirements will consume an increasing share of the US budget.

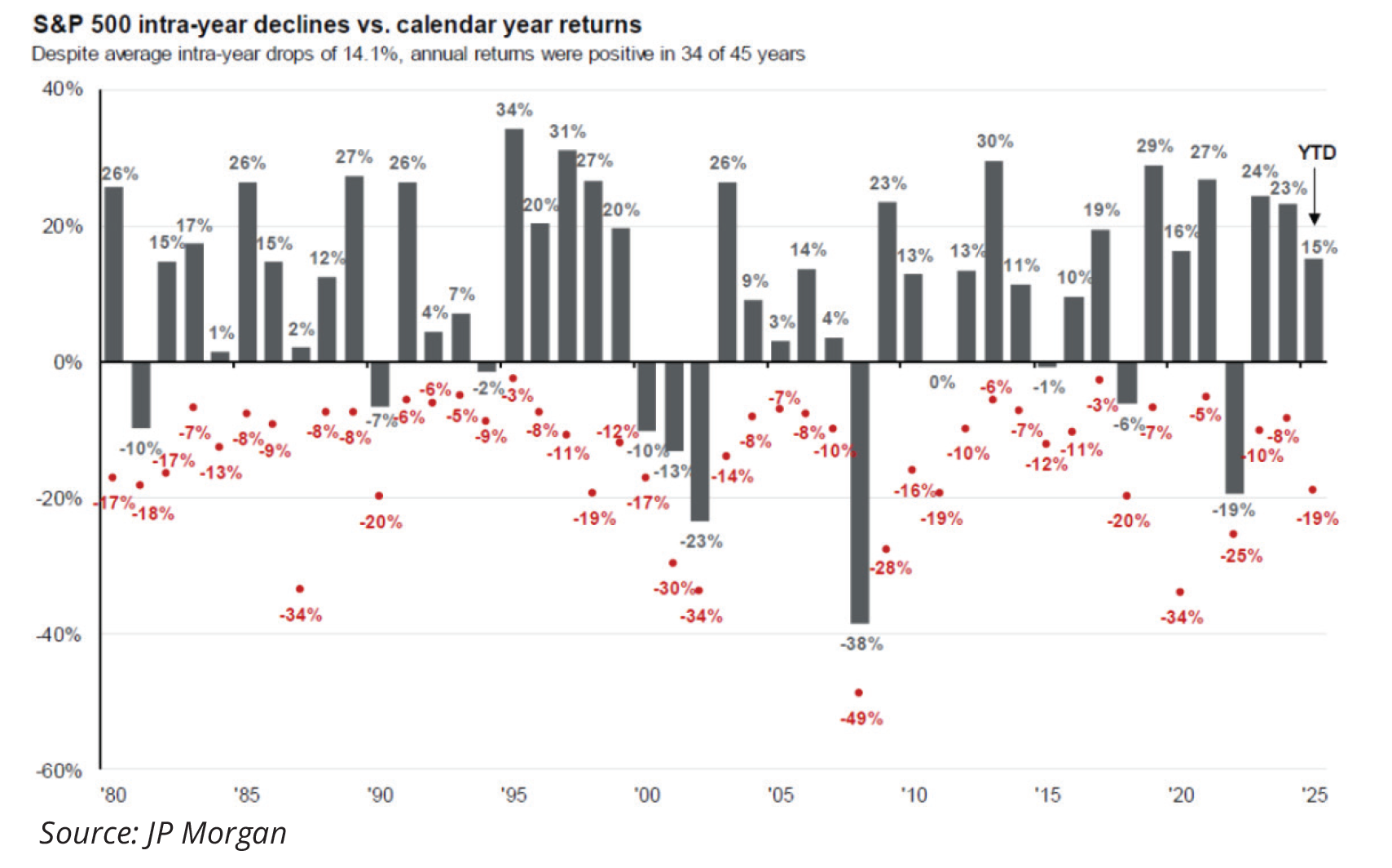

How to manage this uncertainty? One thing not to do is to exit the equity markets entirely. Since 1929: the equity markets have declined by 20% or more 15 times. Investors recouped their investment losses within one year 9 times (of 15) if they did not sell. In 13 out of the 15 bear markets, investors were made whole within two years (frayed nerves notwithstanding). Our belief is that allowing markets time to recover is a core tenet of successful investing. A certain amount of uncertainty and volatility is expected for almost all investment portfolios.

The S&P 500 index declined by almost 19% from February 19th through April 8th 2025 as the tariff program was announced. Once investors were able to understand which tariffs would actually be implemented, the panic abated and the market recovered by 38%. Another tactic that helped many of our clients was diversification. Precious Metals and International Large Cap equities are two sectors where we have maintained healthy allocations for several years. Often these sectors would trail the performance of the US market, but in 2025 for reasons alluded to above, Gold, Silver and International Equities outperformed US stocks and were all major contributors to performance.

In addition to diversification we advocate periodic rebalancing. For example, we reduced our Gold position after a very strong year. Conversely, interest rate pressures have left real estate lagging the overall market; sub-sectors such as office and retail have been weak. We have been focusing on opportunities here as some industrial, data center, and cell tower REITs have seen share price declines seemingly unjustified by their financial results. We believe that the most interest rate sensitive sector - fixed income, should resume its role as a source of stability. The 10 Year US Treasury yield rose from 0.76% in November 2020 to 4.99% in October 2023. This equates to a price decline of about 27% for what is considered a risk-free asset. Interest rates have been moving sideways to slightly lower, which should add a positive tailwind to investor portfolios. Our research indicates that fixed income investments should provide material returns above cash savings and money market products as interest rates continue to decline.

Another powerful tool to help assuage investor unease is to reassess one’s risk profile on a regular basis. One-time events such as employment changes, retirements, and inheritances can often lead to investors taking too much or too little risk. We often ask investors what they would do if the equity markets suddenly sold off by 15%: Sell out? Nothing?

Buy more? If your response is to “Sell out”, we would strongly advocate for a reassessment of your risk profile. We may perceive a sharp decline in markets as a unique investment opportunity, which may be surprising for less experienced investors.

As for where we stand now, we do not think we are at a point of maximum optimism or pessimism. Inflation, income inequality, and high speculative behavior in certain corners of the investment markets are troubling. However Artificial Intelligence is an undeniably deflationary force along with all its promises to enhance worker productivity. The Federal Reserves, Vice Chair, Phillip Jefferson recently opined on the economy and AI;

“AI can allow a worker to complete tasks in moments that previously took many minutes, if not hours. That has caused many to question whether AI will lead to notable job loss. This potential disruption of labor is a real risk. By automating certain tasks, it could lead to a reduction in some types of jobs. But increased productivity leads to economic growth, which may create new employment opportunities. AI is also expected to create new job categories and transform existing ones. There has been robust competition among high-tech firms for workers who possess the skills to develop this technology… There are many examples where transformative technologies, such as the personal computer, did cause some workers to lose their jobs, but we also saw new industries and occupations emerge because of the innovation”.

We take the view that one of the greatest strengths of the US economy is its technology industry and its ability to drive prosperity. We continue to research new developments within the Quantum Computing space and what industries may profitably leverage new AI applications.

It has been said that genius is 1% inspiration and 99% perspiration. We will be on the lookout for inspiration along with everyone else, but we are committed to balancing return opportunities with risk and volatility the markets exhibit. We focus on each client’s needs and we do the necessary work to develop well-diversified and risk appropriate portfolios. Thank you for your continued confidence in our process.