5C Wealth Review and Outlook — May 2026

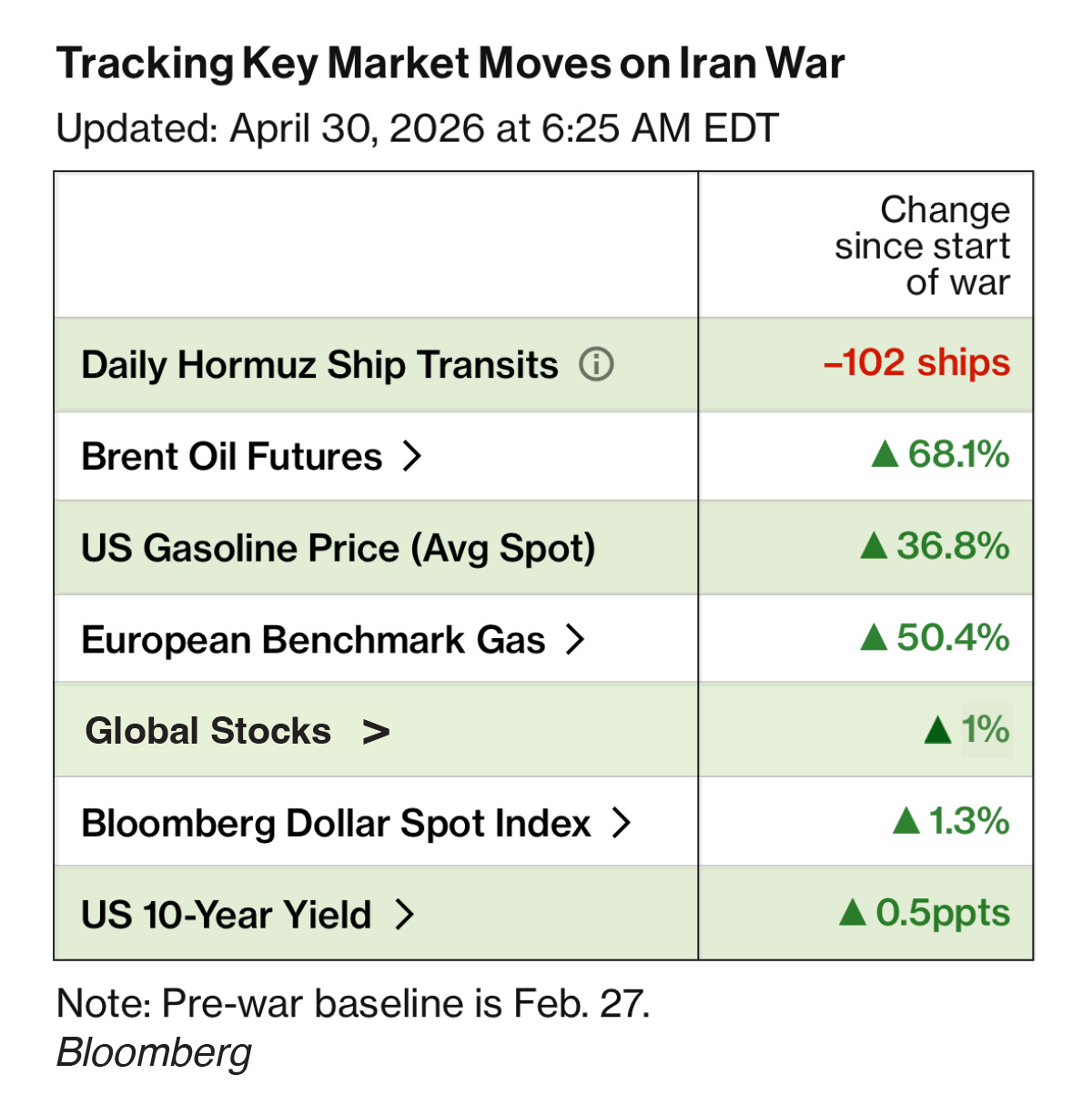

As the Northeastern US fully thawed after an “endless” winter, the Middle East conflict remained white hot without a definite and lasting resolution in sight. We wanted to take this opportunity to discuss how 5C Capital is monitoring and reacting to this situation. The current conflict has clearly caused an uptick in capital markets volatility. The CBOE Volatility Index (“VIX”), the market’s most commonly cited “fear gauge” spiked from below 20 to above 30 shortly after the conflict began. Although the VIX has returned to a more normalized 20 range, we have experienced increased client inquiries regarding the effect of current events on their portfolios.

Clients frequently inquire about portfolio risk and whether they should be “taking some more money off the table” (reducing stock market exposure). They are concerned that the war in Iran will cause elevated energy prices for an extended period. Below is the response we sent early last month:

We wanted to respond quickly to your portfolio risks regarding market concerns caused by the Iran war and all the Geopolitical turmoil in the world.

This is an especially challenging environment in which to invest as the uncertainty is high and the range of outcomes is very wide. Plus, lots of big swings in the markets can be unsettling. The Iran conflict/war has had a massive impact on the global economy as it has caused a sudden sharp rise in the price of energy. Most markets have digested this energy price spike because they consider it short term. For example, oil for delivery at the end of 2026 can be had for about $20 less ($77) than oil for delivery at the end of June ($97). All oil contracts have been trending higher since the war began, but there is still an expectation for prices to come down materially before too long.

We are closely monitoring developments, but feelings and emotions cannot incorporate all the factors that the markets and investors are synthesizing/digesting. Markets are smarter than most of us individually, because they incorporate both positive and negative outcomes. Most of us as human beings tend to focus on the negative (it’s hard wired in our brains this way).

Perspective and patience are key ingredients to investing so we try to incorporate the potential for positive outcomes on the economic front even if there is geopolitical turmoil. One has to be encouraged by some of the data we’re seeing from the economy. We have relatively low unemployment, positive economic growth, and fiscal stimulus just hitting our economy from tax refunds. There are things to worry about, not only geopolitical. There are some cracks emerging in credit markets, with loans to software companies coming under selling pressure. Technology companies are spending ungodly sums to build out AI infrastructure, and it is far from certain how the AI innovations will impact domestic employment levels. Markets have a funny way of climbing a “wall of worry” and discounting several possible negative outcomes.

Our general outlook on the global economy is positive, and we would agree that this market has discounted the war both in terms of its duration and its severity. Given all of this, the most important thing is your comfort around risk and that we have enough liquidity and stability for you. We do not want you or any one of our clients to become panic sellers if things do get worse and the market trades down to lower levels.

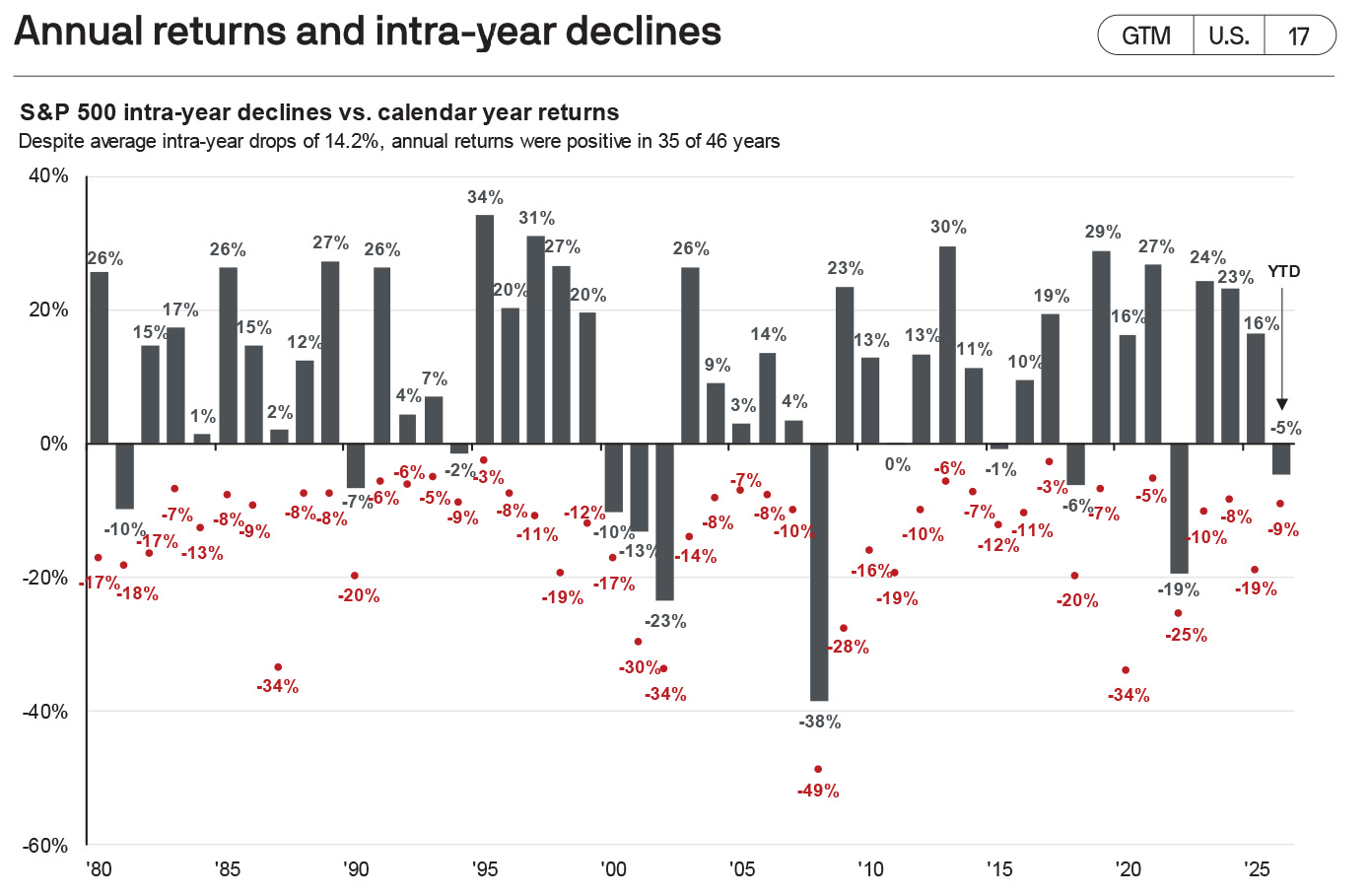

A fruitful meeting with one concerned client shortly followed this communication. We might have also raised the following issue for consideration: Isn’t uncertainty high all the time? Essentially, it is and the market factors it in. The lowest close of the S&P 500 this year was March 30 at 6,343 after a decline of 9%. We have since recovered and then some, as the S&P 500 closed out April at 7,244 for a monthly return of 10.4%. The year-to-date return of 5.3% would be considered above average for most years; despite the geopolitical tumult.

We encourage all clients to contact us for a review of their portfolio and determine whether their current allocation meets their comfort level for risk.

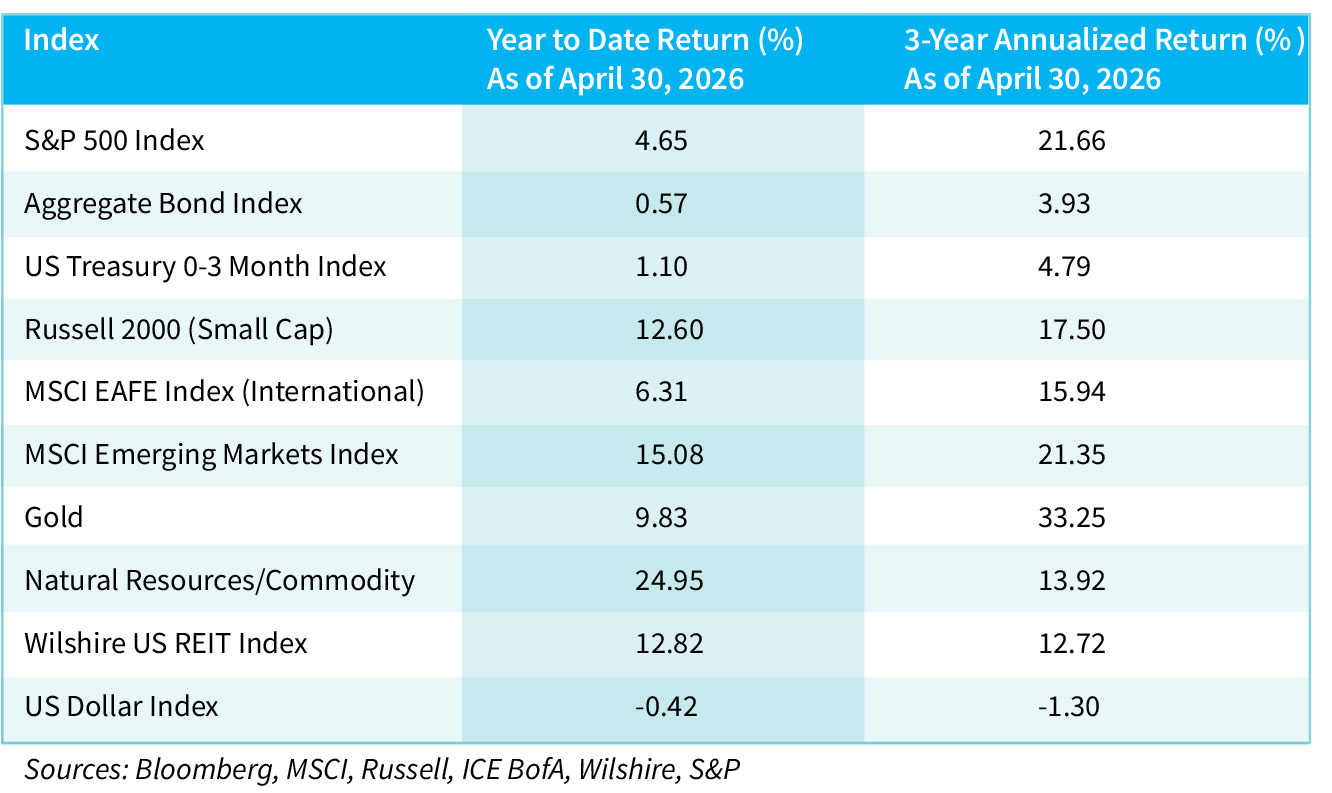

The table below summarizes Global benchmarks and reflect strong capital market returns over these periods.

Dimensional Funds Advisors covered uncertainly in a recent communication:

Investors could benefit from reframing the way they think about uncertainty. This unavoidable aspect of life is often interpreted as a pejorative, “I’m concerned about the political situation or economic outlook and what will happen with my portfolio.” In this view, uncertainty is seen as a threat to one’s invested wealth.

The other side of the argument is that risk and return are related. Bearing the risk of uncertainty is why you get paid a return to be an equity shareholder. And the equity premium is a necessary component for many investors to grow savings to the level needed to eventually retire. So, rather than focusing on the potential for a market downturn—which tends to be temporary anyway—investors should focus on the long-term benefits of embracing uncertainty.

Scott Gallaway, The NYU professor recently wrote:

It’s more interesting, and you sound smarter, to catastrophize vs. articulate the arc of history: Things will likely get a bit better … every day … yawn. But it’s always healthy to ask, “What could go right?

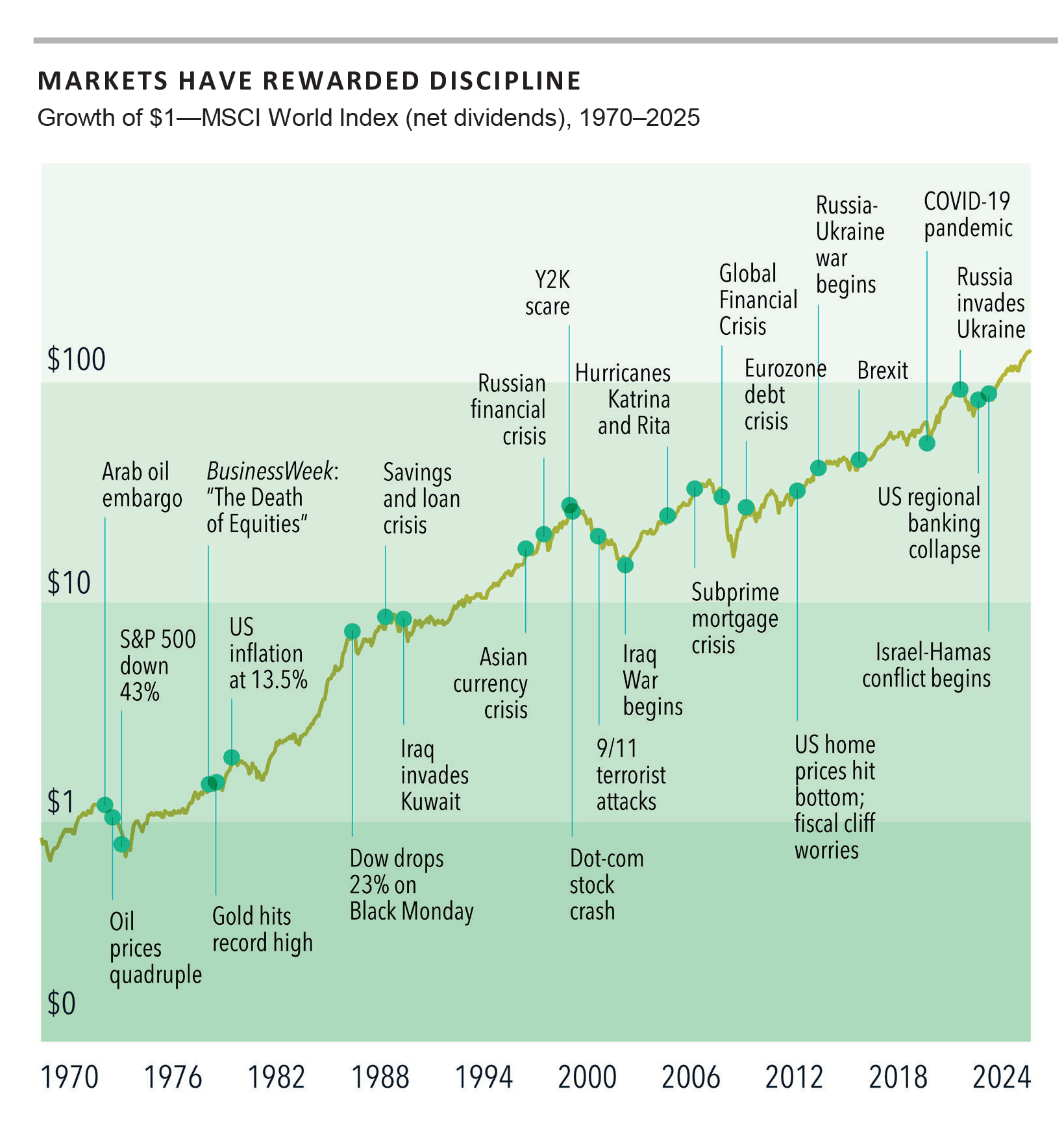

Geopolitical Risk

The chart below depicts the above sentiment. Virtually every year since 1980 has had a substantial drawdown in the S&P 500. If you had extrapolated that negativity going forward, very often you would have missed out on positive annual returns.

Source: JP Morgan

Looking forward, we seek to balance the potential negative impact from higher energy prices, with expected fiscal stimulus from the latest economic legislation. These two forces may essentially cancel each other out; leaving the focus on domestic labor markets. We note that the US’s status as a net energy exporter, may dampen the unpleasant price shock we are currently experiencing. While certainly not pleasant, our increases have been much less severe than countries more dependent on imported energy. We look for this relative trend to continue.

Although new job creation has slowed considerably, the unemployment rate still remains historically low, and wages are growing above the rate of inflation. A continued positive development is that a key leading economic indicator, weekly jobless claims, continues to register at levels around 100,000 fewer than where they’ve been when a recession was imminent. So, for all intents and purposes, the “no-hire, no-fire” economy remains intact.

If the Middle East war moves into a more permanent de-escalation phase, or ends, we would expect energy prices to decline in a measured but deliberate fashion. Although the scope of the disruption has moved higher, and energy prices may need several months to revert back to pre-war levels. Nevertheless, the underpinnings of the U.S. economy came into 2026 on a relatively solid note which should help keep overall economic growth moderately positive.

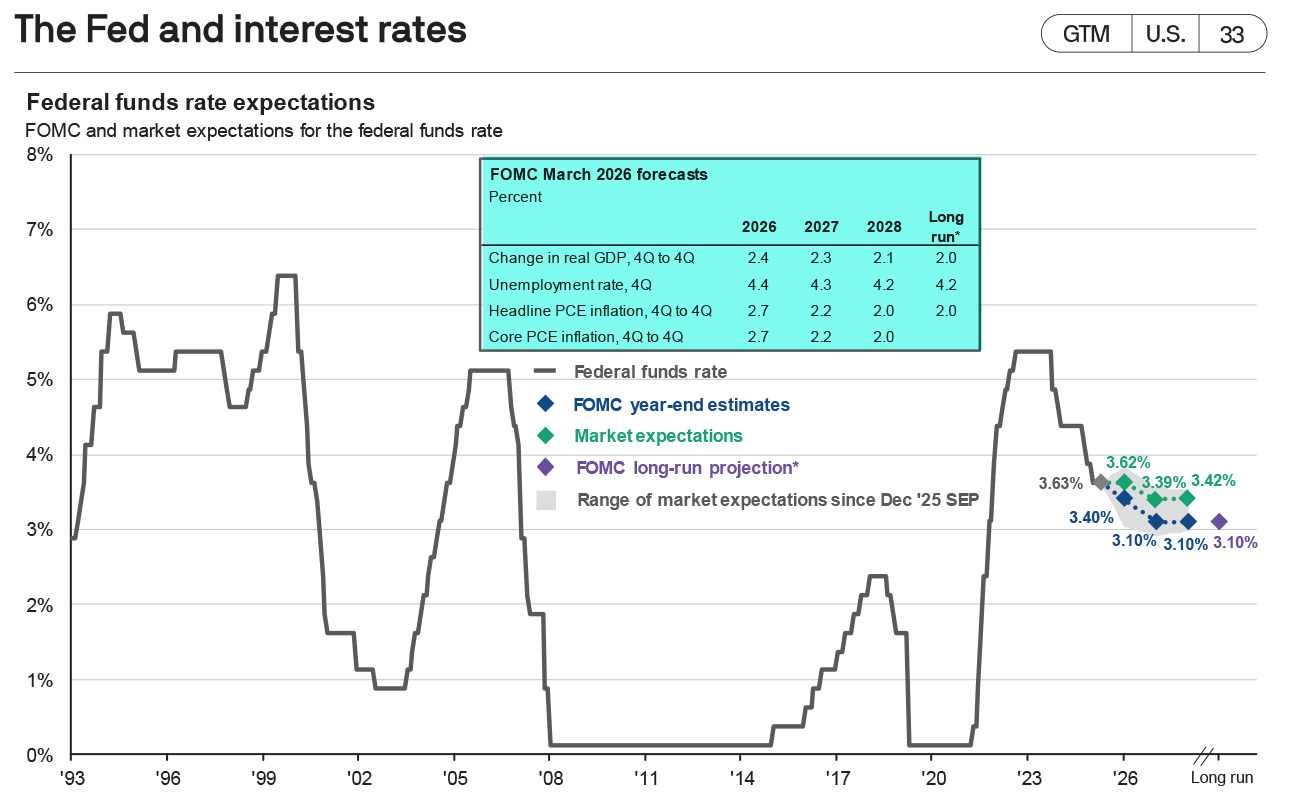

Interest rate markets are pricing in higher inflation due to the war’s supply shocks. Since hostilities began, the 2-Year and 10-Year US Treasury notes have risen in yield by 0.46% and 0.38% respectively; the 30 Year fixed mortgage has increased from 6.12% to 6.38%. The futures market has assigned a greater than 50% chance that there will be one rate hike in calendar year 2026. The chart below depicts these shifts in interest rate outlooks.

Source: Federal Reserve, JP Morgan

Recent weeks have reinforced our conviction that investors should look past today’s headlines, however ominous they may sound. It would be far better to focus on whether the risks you are taking are appropriate for your investment time horizon and objectives, and whether you could benefit from a more diversified portfolio. We at 5C Capital stand ready to assist in these endeavors.