Global capital markets are not experiencing typical summer doldrums. When considering the recent abrupt declines in the global equity indices, one can’t help feeling some degree of uneasiness. With recent stock market highs in July, we were in a benign investing environment where the Federal Reserve was signaling interest rate reductions, and we were on the cusp of an Artificial Intelligence (“AI”) led technological revolution. Seemingly overnight, volatility in Japanese markets spiked, the Fed’s interest rate reductions were now harbingers of trouble. Economic growth appeared to be slowing, perhaps even turning negative, and the AI revolution would be proceeded by immense capital spending with no visibility into the timing of potential returns.

Source: Bloomberg

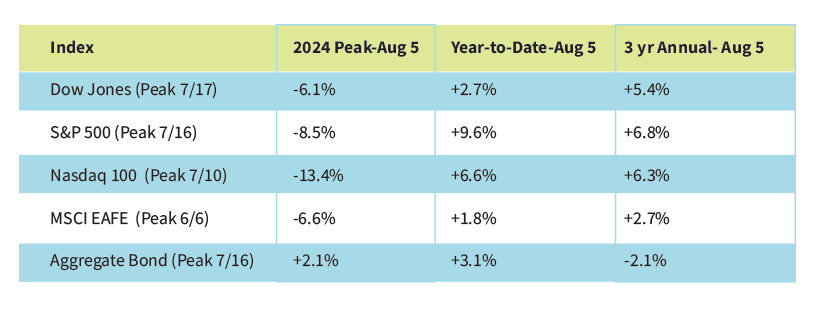

The second column of this table depicts these significant recent moves. However, when incorporating data from longer time periods, the returns begin reverting towards our long-term assumptions. As uncomfortable as these periodic pullbacks may be, they are normal – even “helpful” since they dampen unrealistic expectations. During a much longer period (1984 to 2023), the S&P 500 Index average annual return was 11.3%. Although that implies investors expected similar/consistent 11% annual returns, there were only three years in which the Index returned between 9% and 12% during this period. Volatility is much easier to tolerate when you expect it. We also note the last line of the above table showing the periodic returns of the Aggregate Bond Index. During the recent period of volatility, fixed income investments were relatively resilient and benefitted from declining interest rates. As the market begins to price in the lowering of short-term rates, bonds of all maturities have rallied. The Fed has historically used its powerful tool of monetary policy adjustments, such as lowering the Fed Funds target rate, to counter potential economic slowdowns. We expect the Fed to continue this practice and advocate continued actively managed fixed income portfolios for most investors.

One reason that it’s hard to envision a cataclysmic sell-off akin to that following the Global Financial Crisis of 2008, or 2020’s Pandemic is that we are lacking such a devastating event. Yes, equity returns have been driven by a small group of companies, valuations are at relatively high levels and the unemployment rate is trending higher – however, companies are generally profitable with stable balance sheets. The economy continues to grow, and we are not experiencing significant product shortages. Credit markets are functioning, inflation is stubborn in some areas, but subsiding in others. Considering these factors, we expect equity markets to remain flat the balance of the 2024 with pockets of volatility around major events – the upcoming elections, geopolitical events and abrupt monetary policy changes.

One positive outcome of market volatility is the opportunity to reassess asset allocations and long-term financial plans. Is your current exposure to risk assets appropriate given your needs? Are your cash reserves sufficient to avoid having to sell into weak markets? We encourage you to bring your questions to our team and set aside some time to meet. We wish you an enjoyable and cooler the rest of summer!

Sincerely,

5C Capital Management Investment team